RSS

RSS|

By Mark Melin What is the most effective approach for an investment consultant to evaluate the seemingly ever growing universe of liquid alternative investment managers?

Jason Schwarz, Managing Director with Wilshire Funds Management, recognizes the challenges in evaluating various complex alternative strategies. Wilshire advises on $750Billion in institutional assets.

Given that the hedge fund manager databases only cover about 60% of the universe, investors had to rely on "soft sourcing," according to Jonathan Miles, Vice President and Head of Alternative Strategies with Wilshire. "We have had to attend conferences, ask fellow investors for referrals, and meet regularly with prime brokers. However, today this process is being streamlined by the emergence and rapid growth of liquid alternative funds." "Now the first step becomes the application of quantitative screens since there is a known universe of funds for which data is available," commented Schwarz at a recent liquid alternatives advisor conference. This allows the research process to focus on the heavy lifting of manager due diligence and identifying unique investment opportunities. "Ultimately, we believe that an investor is not buying a fund so much as an investment team and process, and as such, assessing the team is really a qualitative exercise. After the initial filtering stage, we must understand what is fundamentally driving the performance. What is the manager's edge? What is unique about their strategy?" Noting that alpha generation is a zero-sum game, Wilshire Funds Management offers seven critical questions investors should consider when evaluating liquid alternative managers:

Jonathan Miles, Vice President and Head of Alternative Strategies with Wilshire. The firm was founded in 1972 and launched the Wilshire 5000 stock index in 1974.

2) Why do these opportunities exist and is it reasonable to assume they will persist going forward? 3) What are the backgrounds (education and experience) of the key investment professionals? In particular, look for teams with significant experience investing in alternative strategies outside of the mutual fund universe. "Just because a manager has been successful investing in a long only strategy, does not necessarily mean they will add value by introducing a hedging or short component to create an alternative strategy" says James St. Aubin, Portfolio Manager and Vice President at Wilshire Associates. Those with an established hedge fund pedigree may be considered earlier in their fund's life than those without such a background. For instance, an experienced and well known hedge fund manager who launches a mutual fund version of a strategy may receive consideration with just $50 million in assets under management and a one year track record, assuming all other qualitative considerations are met. Meanwhile, an emerging manager with less experience might receive consideration only after three years of solid risk-adjusted performance and $250 million in AUM. 4) Does the firm's ownership structure promote investment team stability and properly align investment professional compensation with risk-adjusted returns? 5) What resources are supporting the strategy? Do they have significant capital to manage both the business and trading operations? 6) Is the investment process disciplined and repeatable? Is the manager able to take advantage of a rich opportunity set by implementing a sound process? 7) Identify the risk management process and seek demonstrated execution. How do they measure and manage risk in their portfolio(s)? How do they size their positions? What is their sell discipline?

James St. Aubin, Portfolio Manager and Vice President at Wilshire Associates, typically might evaluate an emerging manager after three years solid track record and $250 million AUM. Managers with a known reputation and institutional background might receive a look with as low as $50 million under management.

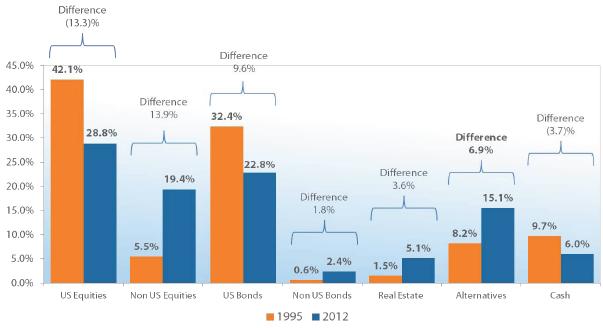

Understanding alternatives is important to consider in an economy that currently appears to be driven by stimulus and quantitative easing, a point of caution expressed by yield curve trader Bob Southhard at the recent JPMorgan Unconstrained Investment conference, which Wilshire attended. Wilshire is quick to note that it has observed a material shift in institutional assets into alternatives, noting that the allocation differential between 1995 and 2012 has been most positive for alternatives and negative for US equities and US bonds. � � � � � � Institutional Trends: Allocations Shifting Towards Alternatives Source: wilshire TUCS

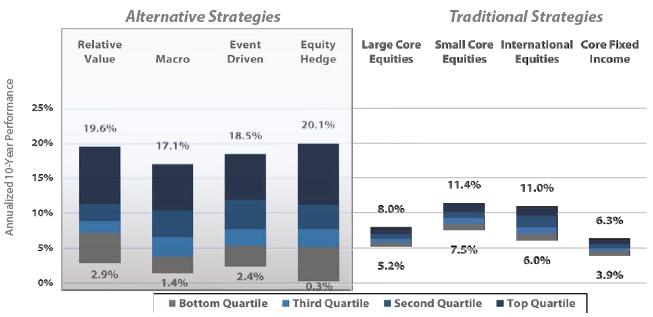

Unlike traditional asset class categories, manager dispersion is much more pronounced among liquid alternative strategies. The key for investors, particularly those utilizing alternative mutual fund products with limited track records, is to use sound due diligence practices to avoid the potential serious negative impact of sub-par managers. "Picking the wrong manager in the alternatives space can be far more costly than doing so on the long-only side," said Mr. St. Aubin. To illustrate the point, Wilshire compared the dispersion in performance between the top 5% to bottom 5% performers in both traditional and alternative manager universes. "The risk of damaging overall portfolio performance with poor manager selection is simply much greater with alternative strategies," continued St. Aubin. "Picking the wrong manager in the alternatives space can be far more costly than doing so on the long-only side" Annualized 10-Year Performance: 1/1/2003 - 12/31/2012

Source: Wilshire CompassSM, PerTrac. Large Core Equities represented by the Lipper Classification "Large-Cap Core Funds", Small Core Equities by "Small-Cap Core Funds", International Equities by the Lipper Objective "International", Core Fixed Income by "Intermediate Investment Grade". Alternative strategy custom peer groups are defined by their respective HFRI benchmark constituents. Dispersion of Manager Returns: Large Spread Between Top and Bottom With respect to manager selection, Mr. Schwarz advises clients to maintain realistic performance expectations through different market environments and through a full market cycle. "Even great managers are not immune from periods of challenging performance. A manager should be able to articulate in which environments they will do well and in which they will struggle," St. Aubin said. While there is certainly a "buyer beware" element to selecting alternative investment strategies, Wilshire believes firmly that this growing trend is overwhelmingly positive for retail investors. "For years, it was only institutional and certain very high net worth investors that had access to hedge funds and other investment strategies that have the potential to provide enhanced portfolio diversification and risk-adjusted returns," Schwarz says. "The growing availability of mutual fund options is now leveling the playing field. However, careful due diligence and understanding what you are getting is key." *As of 12/31/2012. |

|

This article was published in Opalesque Futures Intelligence.

|

{kind=link}